Benner Cycle

The benefit of social media is that it gives everyone a voice. The downside of social media is that it gives everyone a voice. An example of the latter are pseudo finance "influencers" on LinkedIn. You know, those Entrepreneurs|Founders|Futurists|Evangelists that will post an arbitrary graph along with a GPT scripted paragraph of "investment advice" in an attempt to harvest the content machine for engagement. A staple of these trending travesties is a thing called the Benner Cycle.

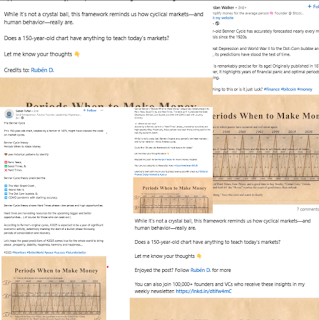

The Benner Cycle is a chart of predicted market cycles that was published by an Ohioan farmer Samuel Benner in his book "Benner's Prophecies of Ups and Downs in Prices", which was published in 1884. This chart is intended to predict market movements from 1924 through to 2059 and is described in the book by Benner as a "sure thing". As you can see in the chart there are two overlapping cycles, a major and a minor cycle. The peaks and troughs are assigned as points A, B and C where C are years when prices are low so you should buy assets, B are years when prices are high so you should sell assets, and A are years when panics will occur so you should definitely sell assets.

I decided to test how accurate the Benner Cycle predictions have been since 1924. Now I know what you are thinking, this is a huge waste of time because all of the people posting it on LinkedIn have surely already done this. It would be crazy to publicly endorse the effectiveness of something without first ensuring its validity. But humour me by pretending we live in a world where engagement is valued over factual information.

I recreated the Benner Cycle graph in Python and overlaid a moving average of the annual return of the Dow Jones Industrial Average. There is some correlation, particularly pre-1940 and the early 2000's, but there are also many periods where market returns do not following the Benner cyclical process. Simply observing the graph doesn't reveal anything about the relationship between the two time series.

I am going to consider Benner's minor cycle only as it conveys more information and the major cycle is mostly a subset of it. The troughs of both cycles are identical and the peaks are almost always identical, only differing by a single year twice and by three years twice.

The minor cycle has two time periods that I will name "favourable" and "unfavourable". Favourable years are those during which Benner predicts it will be good to buy assets. These are denoted as the time periods after points C and before points B on the chart. Unfavourable years are those in which Benner predicts it will be good to sell assets. These are denoted as the time periods after points B and before points C on the chart.

While the scaling of the chart makes these time periods look symmetrical, they are far from it. Analyzing the years 1924 through 2024 inclusive is 101 years. Of these, Benner's chart predicts 67 unfavourable years and only 34 favourable years. During this time period, DJIA showed a positive return 70 times and only had 31 down years.

The Benner Cycle significantly overweights the amount of expected down years. However, we also need to consider the magnitude of returns in each time period. Benner's predicted favourable years have a higher mean and lower volatility than the unfavourable years.

So he was right! His favourable years do make more money and we can now all rebalance our portfolios based on the 150 year old predictions of an Ohoian pig farmer!

What is that weary adage about correlation and causation? Forgetting it leads to the above conclusion and articles like this from Quantara Asset Management. Statistically literacy is low even among people who manage money for a living.

Randomly sampling 34 years from the 101 available and taking the mean has a distribution as below.

The mean returns of the Benner favourable and unfavourable years respectively are marked on the distribution charts. These are towards the tails of their respective distributions they are not the most extreme events seen when randomly sampled. The red line meets the distribution curve at ~3% on the y-axis. This means that if you randomly labelled 34 years as favourable and 67 years as unfavourable then you have a 3% chance of getting the exact same mean return as the Benner cycle.

As these distributions are normally distributed we can directly calculate the probability of getting comparable levels of returns.

Both distributions have comparable means but the 67 year samples have a lower standard deviation due to the law of large numbers.

μ + σ = 10.68, μ + 2σ = 13.34

I include calculations for the 34-year distribution only as the results are the same for both. Benner's favourable years' mean of 13 lies within one and two standard deviations from the mean. This means that if you randomly selected 34 years and took the mean return, 13.6% of the time you would get a value close to 13.

Using a Z-test we can test the hypothesis that a mean of 13% is statistically significant from the mean of a distribution of randomly selected years.

Z = (X - μ) / σ = (13 - 8.02) / 2.66 = 1.87

A Z-test has a critical value of 1.96 for the 5% significance level. As 1.87 < 1.96 we fail to reject the null hypothesis and conclude that a mean of 13% is not statistically significantly different from the population mean of 8%.

Suffice to say, contrary to intuition a 13% return in a selection of 34 years (the favourable years) is not as unusually large as it initially might seem. Benner's favourable years having a higher average return than the unfavourable ones does not infer any information about the correctness of his predictions. Another way to think about this is by considering the unfavourable years that earn 5.5% on average. If his predictions are correct these should be negative. Would you be happy to have sold assets on these years?

We can assess the accuracy of the predictions directly using a confusion matrix. We see that the Benner cycle predicts 55 (29+26) years correctly. From a sample of 101 years this is an accuracy rating of 54.5%. Marginally better than flipping a coin.

Now we want to test how significant that level of accuracy is. For example, Benner predicts 26/(26+5) = 84% of the unfavourable years correctly but only 29/(29+41) = 41% of the favourable years correctly. Given we know that the Benner cycle simply predicts that 67% of years are unfavourable and 33% are favourable, how significant are the above results?

To measure this I used another statistical significance test, Fisher's exact test. This test is used for the analysis of contingency tables so it is perfect for our confusion matrix. It was created by Ronald Fisher after Muriel Bristol claimed she could taste the difference between cups of tea when the milk had been added first or last, known as the lady tasting tea experiment. In our case, the Benner Cycle takes the place of Muriel Bristol in claiming to be able to identify favourable and unfavourable years.

The null hypothesis is that there is no associations between the two binary variables. The output of the test is a p-value that measures the significance of the deviation from the null hypothesis. The categorical data follows a hypergeometric distribution.

The p-value of the above table is 0.0134. This means that there is a 1.34% of getting a table at least as extreme as the one we observed, conditional on the marginals being fixed. This leads to a rejection of the null hypothesis that the two categories of favourable and unfavourable years are independent. It suggests that there is a meaningful level of accuracy in Benner Cycle predictions.

However, a requirement of any independence test is that each individual observation is independent. Whether there each year of DJIA returns are independent is probably a whole are of studey. But as the Benner Cycle is a repeated pattern, each year is not independent of the previous year and the time series is not stationary. Independence significance tests are not to be relied upon for time series data.

Lets leave the world of statistics now and answer the only question that really matters, does using the Benner Cycle make money? Yes, it does. Suppose you invested $1000 in the market in 1924 and followed the Benner Cycle of when to sell assets, that $1000 would be worth over $45000 at the end of 2024. The Benner Strategy also outperforms the inverse Benner Strategy where each year you do the opposite of what the Benner Cycle suggests. It is worth noting that the Inverse Benner Strategy is also profitable however.

However, the limitations of Benner strategy is evident when you compare it to the return of simply holding the market. If you had invested $1000 in the market in 1924 and left it there it would have been worth $445000 at the end of 2024.

The biggest downfall of the Benner Strategy is the missed compounding opportunity as a result of the amount of incorrectly identified unfavourable years. The Benner Cycle gets penalized for expecting 67% of years to be unfavourable to hold assets when 70% of years in show positive returns. It is 10x more profitable to stay in the market and take drawdowns than to adjust your portfolio based on the Benner Cycle. Supporters of this psuedo analysis claim that it is expected for the Benner Cycle to be off by a year or two. It is the overall trend of each period that counts rather than the year the market tops or bottoms. So one should follow this chart of market timing, but not be worried when the timing is wrong? The human ability to hold contradicting beliefs never ceases to amaze. But I redid the analysis in this blog for average period return rather than yearly return and received the same results. You can check it on my github if interested.

Comments

Post a Comment